43 duration of a coupon bond

BondView Glossary | Duration Coupon rate: A bond's payment is a key factor in calculating duration. If two otherwise identical bonds pay different coupons, the bond with the higher coupon ... Bond Duration | Formula | Excel | Example - XPLAIND.com Example. On 14 November 2017, you added the three bonds to your company's investment portfolios: (a) a $1,000 zero-coupon bond yielding 5.1% to maturity which is 31 December 2020, (b) a $100 face-value 6% semi-annual bond maturing on 30 June 2023 and yielding 4.8% and (c) a $1,000 face value 5.5% semi-annual bond maturing on 30 June 2023 and ...

What is the duration of a bond? and How to Calculate It? The duration of a bond represents the relationship between the price of a bond and interest rates. Generally, the relationship between the two is inverse, which means when interest rates are high, the price of the bond will fall and vice versa. The duration of a bond is different from its maturity as both present different time periods of a bond.

Duration of a coupon bond

How to Calculate the Price of Coupon Bond? - WallStreetMojo = $838.79. Therefore, each bond will be priced at $838.79 and said to be traded at a discount (bond price lower than par value) because the coupon rate Coupon Rate The coupon rate is the ROI (rate of interest) paid on the bond's face value by the bond's issuers. It determines the repayment amount made by GIS (guaranteed income security). Coupon Rate How to Calculate Bond Duration - wikiHow Bond duration is a measure of how bond prices are affected by changes in interest rates. This can help an investor understand a bond's potential interest rate risk. In other words, because bond prices move inversely to interest rates, this measure provides an understanding of how badly the bond's price might be affected if interest rates were to increase. Understanding Duration | BlackRock • The duration of any bond that pays a coupon will be less than its maturity, because some amount of coupon payments will be received before the maturity date. • The lower a bond's coupon, the longer its duration, because proportionately less payment is received before final maturity. The higher a bond's coupon, the shorter its duration, because proportionately more payment is received before final maturity.

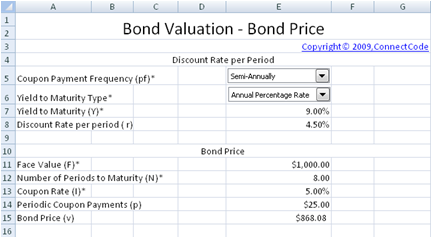

Duration of a coupon bond. Coupon Bond - Guide, Examples, How Coupon Bonds Work Let's imagine that Apple Inc. issued a new four-year bond with a face value of $100 and an annual coupon rate of 5% of the bond's face value. In this case, Apple will pay $5 in annual interest to investors for every bond purchased. After four years, on the bond's maturity date, Apple will make its last coupon payment. Bond duration - Wikipedia In finance, the duration of a financial asset that consists of fixed cash flows, such as a bond, is the weighted average of the times until those fixed cash flows are received. When the price of an asset is considered as a function of yield, duration also measures the price sensitivity to yield, the rate of change of price with respect to yield, or the percentage change in price for a parallel shift in yields. The dual use of the word "duration", as both the weighted average time until repayment Duration of Bonds | Premium Bonds - PFhub Duration of bond = (Bond Price when interest rate increases - Bond Price when interest rate decreases) / (2 x Initial Bond Price x Change in interest rate) Duration of bond can be visualized as a seesaw with a fulcrum whose position when changed balances the payments' present values and the bond's principal payment. Factors that Affect Duration Bond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

Coupon Bond - Investopedia This means the investor gets $50, the face value of the bond derived from multiplying $1,000 by 0.05, every year. For the investor to claim his interest on the bond, he simply takes the... Duration & Convexity - Fixed Income Bond Basics | Raymond James The duration of a bond will be higher the lower its coupon. Duration will be higher the lower its yield. Duration will also be higher the longer its maturity. The following scenarios of comparing two bonds should help clarify how these three traits affect a bond's duration: If the coupon and yield are the same, duration increases with time ... Bond Duration: Everything You Need to Know - SmartAsset How Coupon Rate Impacts Duration. Coupon rate is the interest yield of a bond. This is an annual rate. So if you have a $1,000 bond with a 5% coupon, you will earn $50 of interest from the bond each year (5% of $1,000). A bond will pay this amount in addition to its par value. Bond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. Simply enter the following values in the calculator:

What Is Duration of a Bond? - TheStreet Definition - TheStreet Zero-Coupon Bonds. The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity. What Is the Coupon Rate of a Bond? - The Balance Maturity dates on zero coupon bonds tend to be long term, often not maturing for 10, 15, or more years. 1 Though zero coupon bonds do not pay any interest, by looking at what you paid for it, the maturity value, and the duration of the bond, you can reverse engineer the equivalent of an annual interest rate. Duration: Understanding the Relationship Between Bond Prices … Investment professionals rely on duration because it rolls up several bond characteristics (such as maturity date, coupon payments, etc.) into a single number that gives a good indication of how sensitive a bond's price is to interest rate changes. For example, if rates were to rise 1%, a bond or bond fund with a 5-year average duration would likely lose approximately 5% of its value. Bond Duration: What It Is and Why It Matters - Oblivious Investor A 5-year corporate bond with a higher yield will have an even shorter duration. For example, if sold for face value, a 5-year bond with a 5% coupon rate would have a duration of 4.49 years. Despite having the same maturity as the lower-yielding Treasury bond, it has a shorter duration. The reason for this is that a larger portion of the bond ...

Which of the following are true for a coupon bond a When the coupon ...

What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium.

Solved: 6. Consider A Bond With An 8% Coupon Rate. Your Bo... | Chegg.com

What is the duration of the coupon bond? - koniukhchaslau.com Coupon bond duration: how to determine the investment payback period Coupon bond duration is an important point in an investor's work. This concept represents a certain period of time during which it will be possible to return the funds invested in securities.

Coupon Payment Of A Bond Calculator ~ coupon

Duration - 5minutefinance.org: Learn Finance Fast The Duration of a zero-coupon bond is the number of years until maturity. Also note, we can calculate the duration of a bond portfolio as the weighted average ...

Post a Comment for "43 duration of a coupon bond"