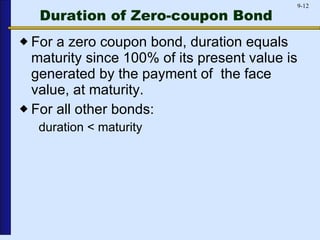

39 duration zero coupon bond

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years. Convexity of a Bond | Formula | Duration | Calculation - WallStreetMojo The duration of the zero-coupon bond which is equal to its maturity (as there is only one cash flow) and hence its convexity is very high; While the duration of the zero-coupon bond Zero-coupon Bond In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued at a ...

Duration and Zero Coupon Bonds - YouTube Examples of Macaulay duration are given for zero coupon bonds.

Duration zero coupon bond

The One-Minute Guide to Zero Coupon Bonds | FINRA.org Zeros, as they are sometimes called, are bonds that pay no coupon or interest payment. will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond ... What is the duration of a zero coupon bond? - Quora What is the duration of a zero coupon bond? - Quora Answer (1 of 12): Everyone is telling you that duration is a weighted average of time until you get the cash flows. That is a bad way to think about duration. It is a measure of risk. The Macaulay Duration of a zero is the time to maturity. The Modified Duration is a better measure. How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816) The present value of the cash flow from the bond is 816, this is what the investor should be prepared to pay ...

Duration zero coupon bond. PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of Modified Duration - Overview, Formula, How To Interpret Below is an example of calculating Macaulay duration on a bond. Example of Macaulay Duration. Tim holds a 5-year bond with a face value of $1,000 and an annual coupon rate of 5%. The current rate of interest is 7%, and Tim would like to determine the Macaulay duration of the bond. The calculation is given below: The Macaulay duration for the 5 ... Duration for a zero-coupon bond.xlsx - Table of Content... View Duration for a zero-coupon bond.xlsx from BUSINESS 200916 at Western Sydney University. Table of Content Zero Coupon Bond Price Duration and Convexity Exercise Strictly Confidential Notes This Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

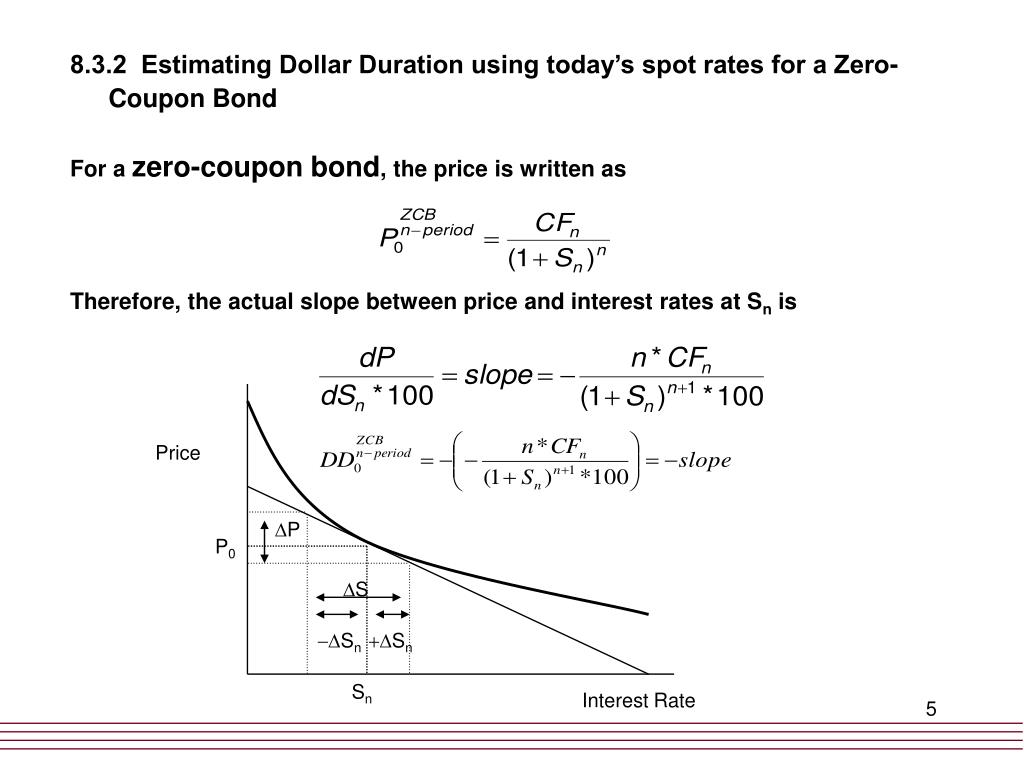

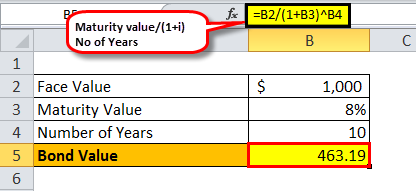

What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... Mr. Tee is looking to purchase a zero-coupon bond with a face value of $50 and 5 years till maturity. The interest rate on the bond is 2% and will be compounded annually. In the scenario above, the face value of the bond is $50. However, to calculate the price that needs to be paid for the bond today, the following formula is used: › zero-coupon-bondZero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far. duration of zero coupon bonds | Forum | Bionic Turtle The Macaulay duration of a zero-coupon bond equals its maturity, such that the Mac duration of a zero-coupon bond must be monotonically increasing, and. DV01 = Price * Mod duration /10000, where in the case of a zero coupon bond: Price is a decreasing function of maturity (i.e., a zero is acutely "pulled to par"), but Mod duration is an ... Dollar Duration - Overview, Bond Risks, and Formulas Dollar duration can be applied to any fixed income products, including forwarding contracts, zero-coupon bonds, etc. Therefore, it can also be used to calculate the risk associated with such products. Summary Dollar duration is the measure of the change in the price of a bond for every 100 bps (basis points) of change in interest rates.

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months. › fixed-income-bonds › durationDuration: Understanding the relationship between bond prices ... Duration is expressed in terms of years, but it is not the same thing as a bond's maturity date. That said, the maturity date of a bond is one of the key components in figuring duration, as is the bond's coupon rate. In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. Zero Coupon Bond Calculator - Nerd Counter Zero Coupon bond is also named as accrual bond and it lacks the coupons or the installments procedure for making the payments; instead, a single payment at the level of maturity (the time period or the duration) is paid. The amount that one pays at maturity level is called face value or par value. How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816) The present value of the cash flow from the bond is 816, this is what the investor should be prepared to pay ...

Duration and Zero Coupon Bonds - YouTube

What is the duration of a zero coupon bond? - Quora What is the duration of a zero coupon bond? - Quora Answer (1 of 12): Everyone is telling you that duration is a weighted average of time until you get the cash flows. That is a bad way to think about duration. It is a measure of risk. The Macaulay Duration of a zero is the time to maturity. The Modified Duration is a better measure.

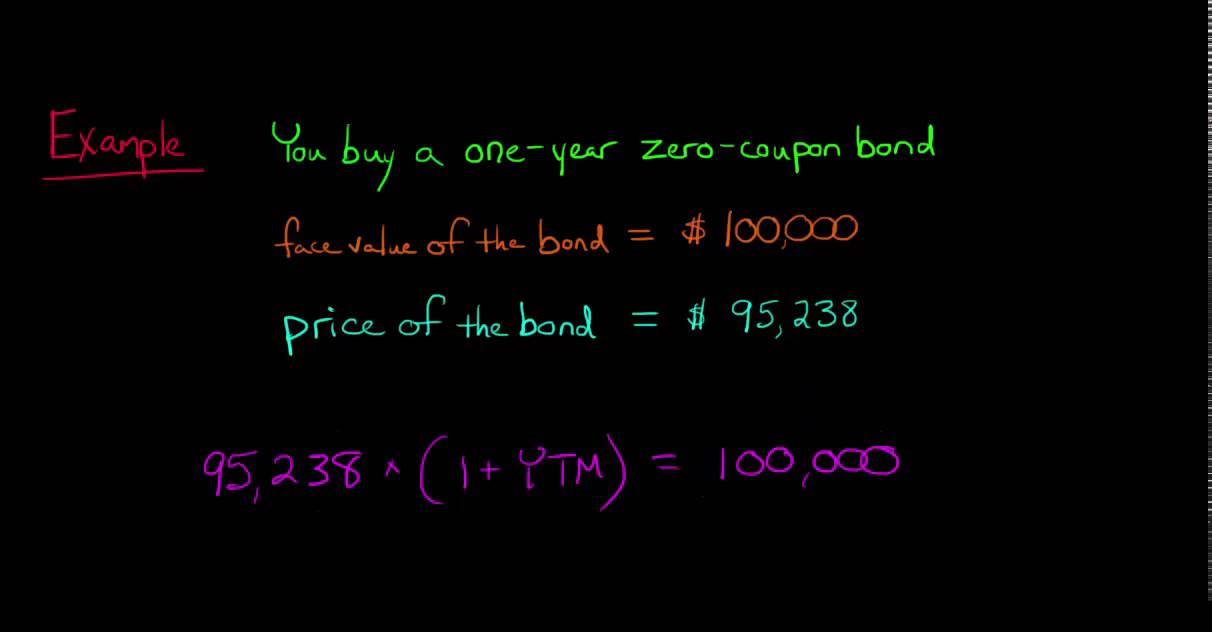

How to compute the YTM of a zero-coupon bond

The One-Minute Guide to Zero Coupon Bonds | FINRA.org Zeros, as they are sometimes called, are bonds that pay no coupon or interest payment. will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond ...

Duration Dv01 Maturity And Coupon A Graphical Analysis - Term ...

Solved] You are managing a portfolio of $1.3 million. Your ...

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

Zero Coupon Bond Valuation using Excel

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Modified duration of zero-coupond bond (FRM practice question)

Duration and Convexity

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

Zero-Coupon Bonds: Characteristics and Examples

Are there bonds with zero duration? - Quora

Answered: An 11-year maturity zero-coupon bond… | bartleby

Actuarial Exam 2/FM Prep: Find Term Structure for Zero Coupon Bonds Given "Ordinary" Bond Info

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

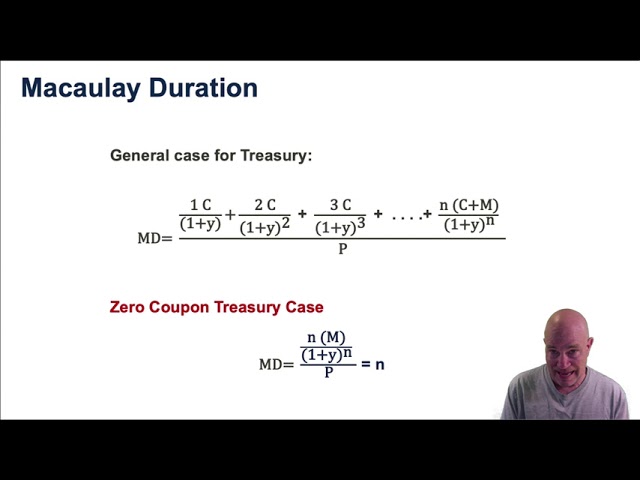

Macaulay Duration

4 Measuring Interest-Rate Risk: Duration

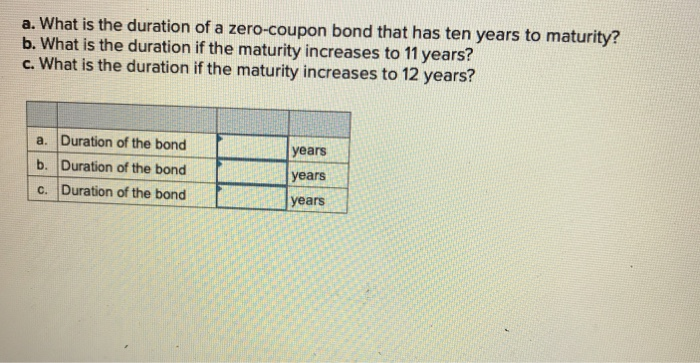

Solved a. What is the duration of a zero-coupon bond that ...

Advanced Bond Concepts: Duration | The Financial Engineer

Duration and Convexity, with Illustrations and Formulas

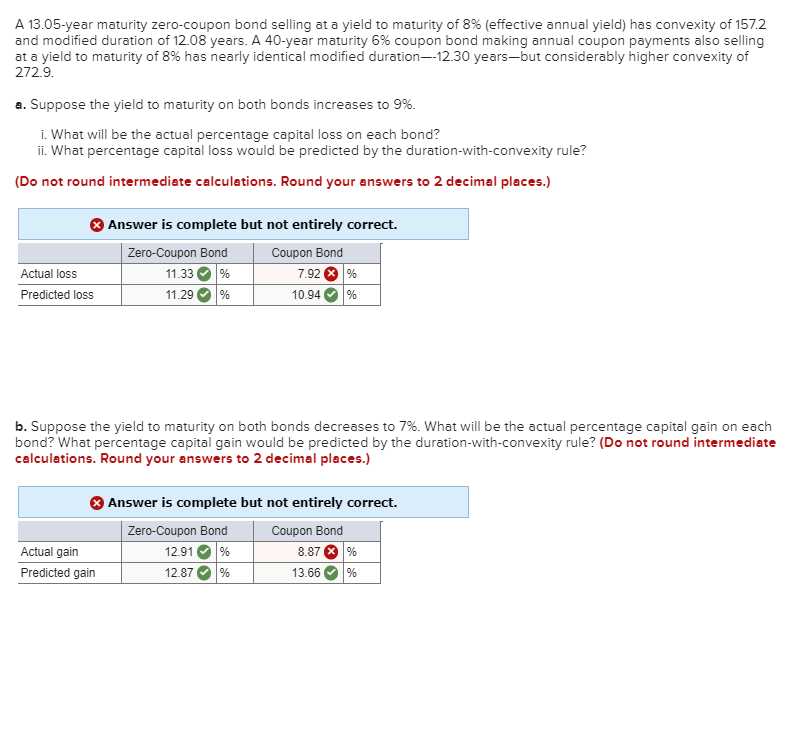

Solved A 13.05-year maturity zero-coupon bond selling at a ...

Valuing a zero-coupon bond | Mastering Python for Finance ...

Zero-Coupon Bond Definition & Meaning in Stock Market with ...

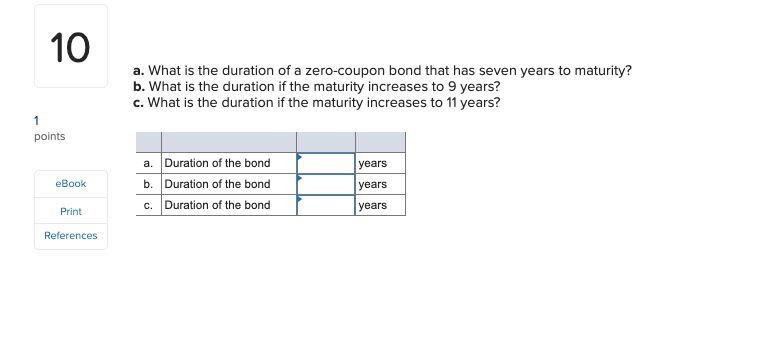

Solved a. What is the duration of a zero-coupon bond that ...

Duration and Zero Coupon Bonds - YouTube

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Convexity of a Bond | Formula | Duration | Calculation

Zero Coupon Bond - QS Study

Calculating the Yield of a Zero Coupon Bond

Aha! Interest rates do matter.

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Portfolio Duration and its Limitations | CFA Level 1 ...

Duration model

Under the Hood: What You Need to Know About Bond Duration and ...

Reserve Bank of India - Database

WWWFinance - Bond Valuation: Campbell R. Harvey

Duration and Convexity in Bond market

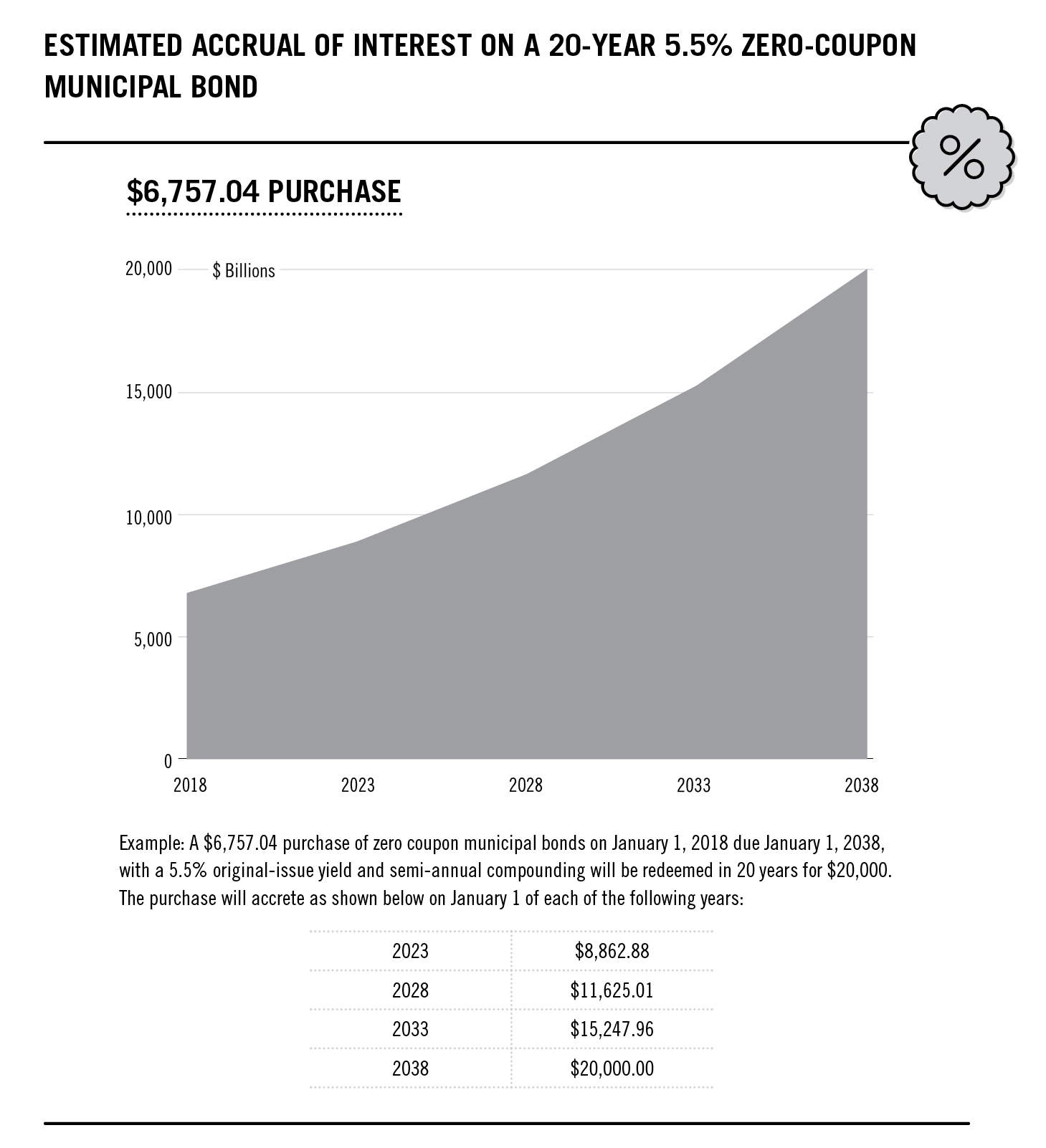

Investor's Guide to Zero-Coupon Municipal Bonds | Project ...

Post a Comment for "39 duration zero coupon bond"