43 what is the duration of a zero coupon bond

Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia 31/01/2022 · If a zero-coupon bond is purchased for $1,000 and given away as a gift, the gift giver will have used only $1,000 of their yearly gift tax exclusion. The recipient, on the other hand, will receive ... Convexity of a Bond | Formula | Duration | Calculation While the duration of the zero-coupon bond Zero-coupon Bond In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued at a discount to its par value and does not pay periodic interest. In other words, the annual implied interest payment is included into the face value of the bond, …

Bond Convexity Calculator: Estimate a Bond's Yield ... - DQYDJ Bond Price vs. Yield estimate for the current bond. Zero Coupon Bonds. In the duration calculator, I explained that a zero coupon bond's duration is equal to its years to maturity. However, it does have a modified (dollar) duration and convexity. Zero Coupon Bond Convexity Formula. The formula for convexity of a zero coupon bond is:

What is the duration of a zero coupon bond

The One-Minute Guide to Zero Coupon Bonds | FINRA.org zero-coupon bond on the secondary market will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond with a face value of $10,000. After 20 years ... ZROZ PIMCO 25+ Year Zero Coupon US Treasury Index ETF - ETF.com Learn everything about PIMCO 25+ Year Zero Coupon US Treasury Index ETF (ZROZ). Free ratings, analyses, holdings, benchmarks, quotes, and news. Zero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far.

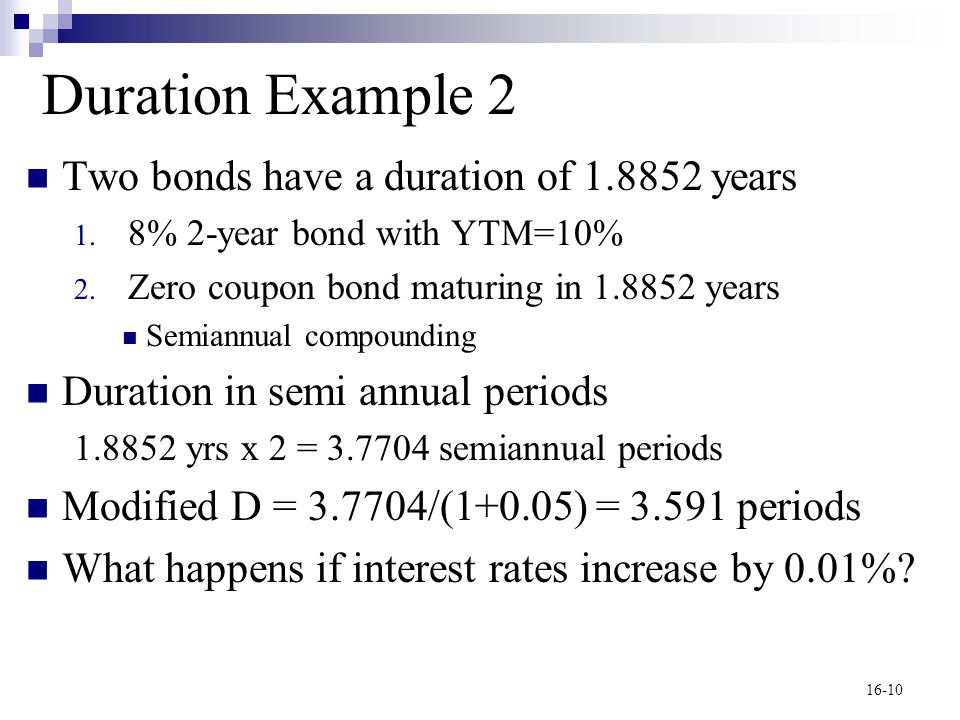

What is the duration of a zero coupon bond. Duration Definition and Its Use in Fixed Income Investing Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ... Bond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ... Bond Present Value Calculator Bond Present Value Calculator. Use the Bond Present Value Calculator to compute the present value of a bond. Input Form. Face Value is the value of the bond at maturity. Annual Coupon Rate is the yield of the bond as of its issue date. Annual Market Rate is the current market rate. It is also referred to as discount rate or yield to maturity ... Zero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far.

ZROZ PIMCO 25+ Year Zero Coupon US Treasury Index ETF - ETF.com Learn everything about PIMCO 25+ Year Zero Coupon US Treasury Index ETF (ZROZ). Free ratings, analyses, holdings, benchmarks, quotes, and news. The One-Minute Guide to Zero Coupon Bonds | FINRA.org zero-coupon bond on the secondary market will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond with a face value of $10,000. After 20 years ...

Price of a defaultable zero coupon bond price in each time t ...

Duration and Zero Coupon Bonds - YouTube

Coupon Bond Formula | How to Calculate the Price of Coupon Bond?

What is the duration of a zero-coupon bond that has eight ...

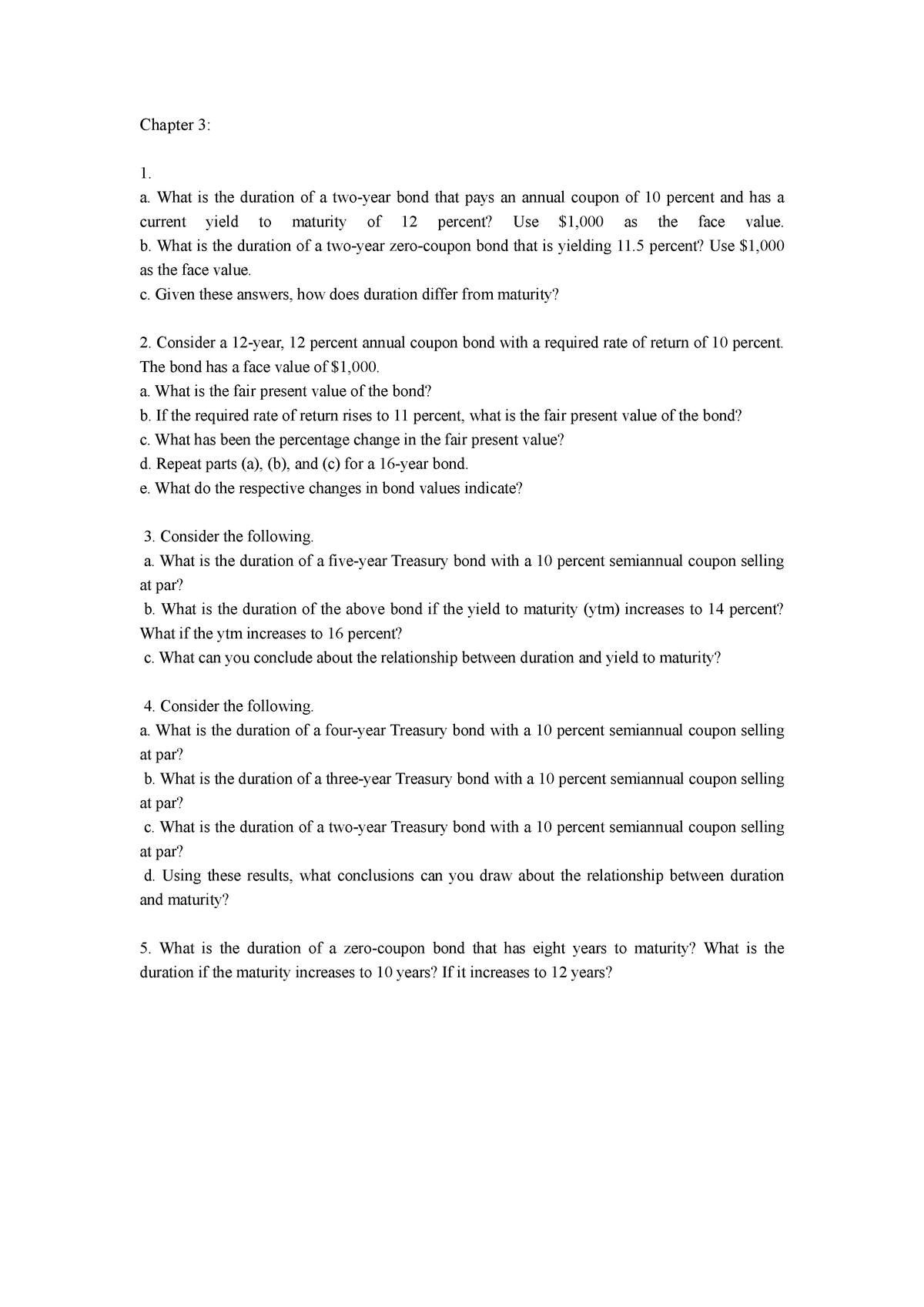

Chapter 3 - Questions - Chapter 3: a. What is the duration of ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

SOLVED:Unvolve zero-coupon bonds. A zero-coupon bond is a ...

Convexity of a Bond | Formula | Duration | Calculation

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents

Modified duration of zero-coupond bond (FRM practice question)

I want to know stochastic derivation of zero coupon bond ...

Aha! Interest rates do matter.

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

Zero Coupon Bonds Explained (With Examples) - Fervent ...

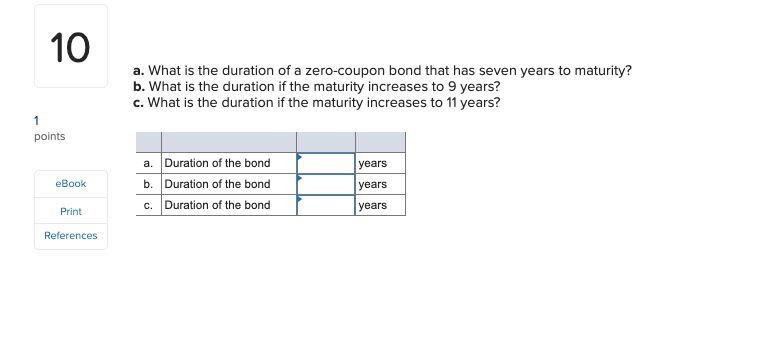

Solved a. What is the duration of a zero-coupon bond that ...

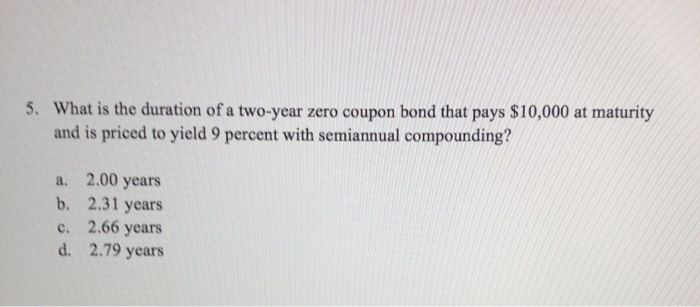

Solved 5. What is the duration of a two-year zero coupon ...

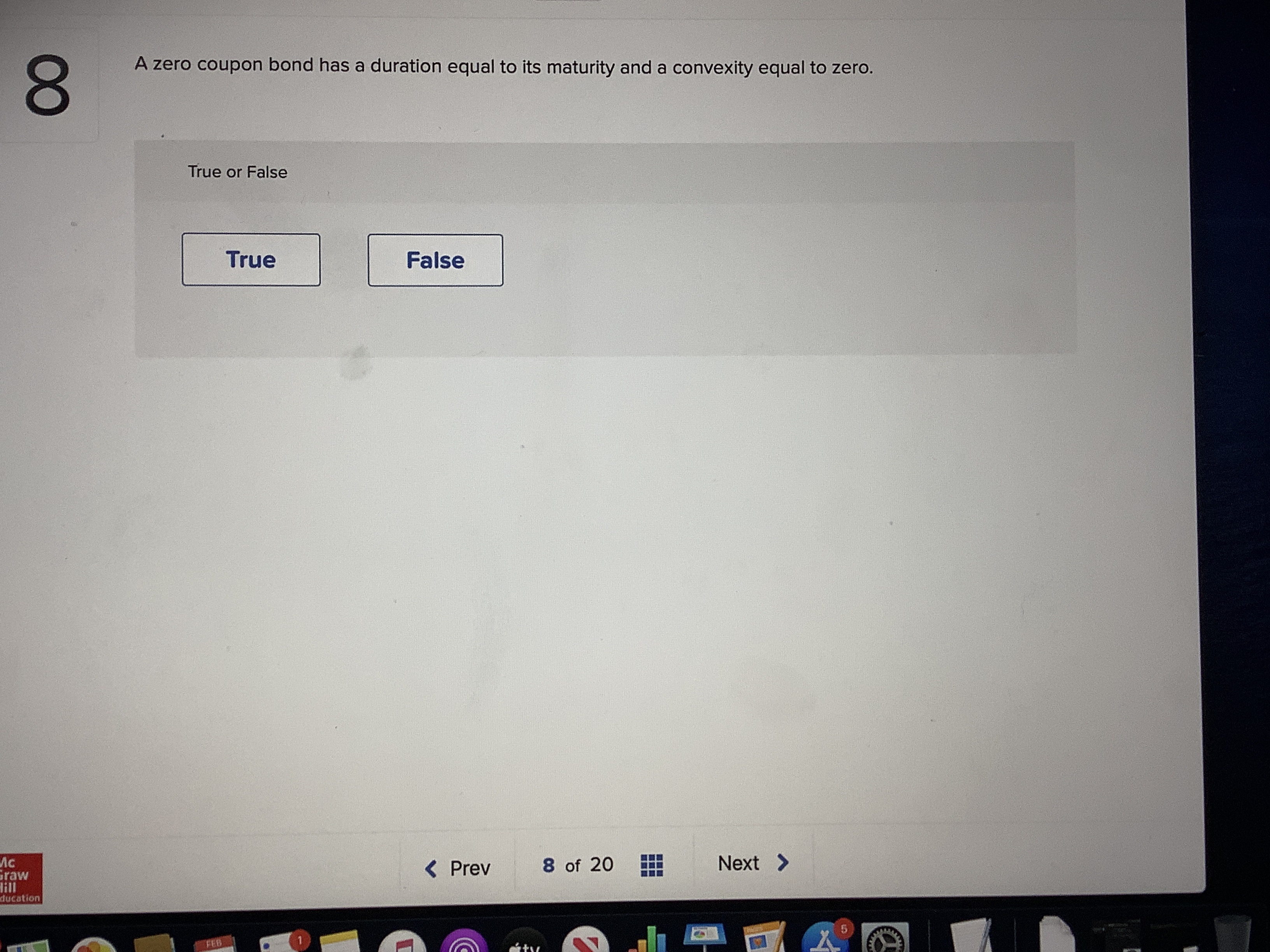

Answered: A zero coupon bond has a duration equal… | bartleby

Zero-coupon bond price as a function of time to maturity for ...

VALUING BONDS

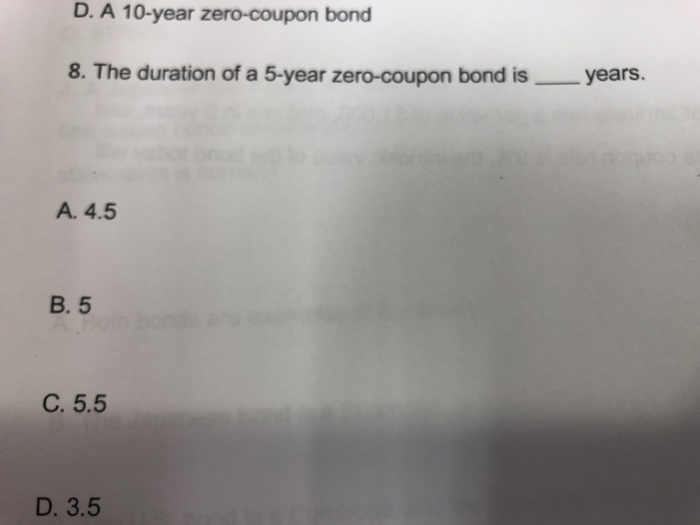

Solved D. A 10-year zero-coupon bond 8. The duration of a ...

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

Zero-Coupon Bond - an overview | ScienceDirect Topics

Chapter 11 - Duration, Convexity and Immunization

Advanced Bond Concepts: Duration | The Financial Engineer

Solved a. What is the duration of a zero-coupon bond that ...

Pricing Coupon Bond Options and Swaptions under theTwo-Factor ...

Bond duration - Wikipedia

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

SOLVED:Unvolve zero-coupon bonds. A zero-coupon bond is a ...

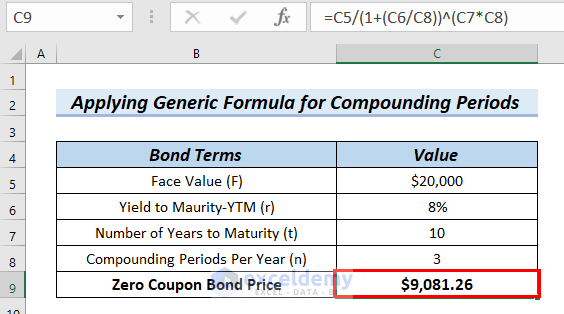

Zero Coupon Bond Price Calculator Excel (5 Suitable Examples)

Yields & Prices: Continued - ppt video online download

Bond Economics: Primer: Par And Zero Coupon Yield Curves

Zero Coupon Bonds

problems 6366 involve zero coupon bonds a zero coupon bond is a bond that is sold now at a discount

Modified Duration - Zero Coupon Bond Modified Duration ...

Solved] You are managing a portfolio of $3.0 million. Your ...

Duration model

Zero Coupon Bond Introduction · Fixed Income

Post a Comment for "43 what is the duration of a zero coupon bond"